A Guide to Tax on Furnished Holiday Lets

A Guide to Tax on Furnished Holiday Lets

September 20, 2021 | Podcasts

Although buy-to-let properties are still a mainstream form of investment, many also make decent profits from furnished holiday lets (FHL). Residential lets and FHLs are distinctly different, not only by how they are legally defined, but also how they are treated for tax purposes. Once you have considered tax on furnished holiday lets the differences, you’ll be able to determine which is more suitable for you.

What is a furnished holiday let?

FHLs are self-contained properties which are let to tenants on a limited time basis of no more than 31 days. They must be self-catered, as well as the facilities which enable tenants to cater for themselves. Accommodation such as B&Bs and hostels are therefore not the same as FHLs. Airbnb is perhaps one of the best-known online platforms that offer users the chance to advertise their FHL or find one to rent.

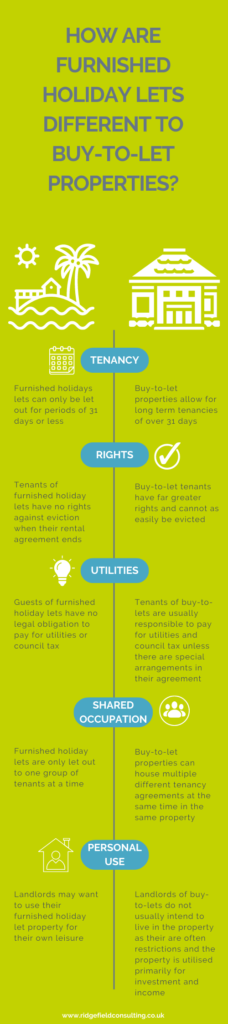

How are furnished holiday lets different to buy-to-let properties?

FHLs are different to buy-to-let properties in many ways:

- Buy-to-let properties usually allow for tenants to occupy the premise for much longer than 31 days.

- Tenants have far greater rights during their occupancy of a buy-to-let property than FHLs, such as the high level of protection they have over eviction, whereas guests of FHLs have no rights to remain after their stay.

- Tenants are usually responsible for paying for utilities and council tax of the buy-to-let property they are renting, unless there are special arrangements in place as part of their rental agreement, whereas tenants of FHLs have no such obligations.

- Many buy-to-lets can be offered as shared accommodation with different tenancy agreements and multiple tenants occupying the same property at the same time. FHLs are only let to one group of tenants at a time.

- In most cases, landlords have no intention of living in or using the buy-to-let properties themselves (many buy-to-let mortgages will restrict this from happening), but with FHLs many owners will use the property as their own holiday home as well.

What qualifies as a furnished holiday let?

For your property to qualify as an FHL it will need to meet all the following conditions:

- Be located in the UK or any other European country

- Be sufficiently furnished (although no items of furniture have been specified, tenants should have enough to cater for themselves)

- Be available to rent to the public for at least 210 days in a year

- Be let out for at least 105 days in a year

- Not be let out to long-term tenants for more than 155 days a year (if you have someone who is regularly renting long periods of time at your FHL, it cannot total more than 155 days a year)

- Must be let out commercially at market rate (if you let out your FHL to friends and family at a reduced rate, this will not count to the 105 days it needs to be let in a year).

If you do not meet all these conditions in any given year, your property ceases to be an FHL for that year but can qualify as an FHL in the following years so long as it meets the qualifying requirements. If your property has not met the occupancy conditions specifically, you may be able to make an election.

What is a furnished holiday let election?

An election allows your property to still be considered as an FHL where it does not meet the occupancy rules in a particular year. If you have more than one FHL, you can use an averaging election which means all your FHL will share an average letting rate. Alternatively, you can also use a period of grace election so long as your FHL met all the conditions and occupancy requirements in previous years. The period of grace election can only be applied for the following two years that your FHL does not qualify and must be made in the first year that it falls short of the occupancy levels. If it continues not to qualify for a third year then the grace period election can no longer be made, but you may still be able to use the averaging election.

How to save tax on furnished holiday lets

One of the reasons FHLs can be as profitable, if not more so, than buy-to-let properties is that there are more tax relief options available:

- Claim for initial expenditure. Initial expenditure is the money you may have to spend before your FHL is rented out. Whilst buying the property itself will not qualify as initial expenditure, fees such as insurance or advertising will be covered as well as costs such as new carpets. To be able to claim initial expenditure, the expenses must have been incurred within the 7 years prior to the date you begin renting out your FHL. By claiming initial expenditure, you will be able to reduce your tax on the earnings from your FHL.

- Being able to offset your mortgage interest payments against your rental income. If you took out a mortgage to purchase your FHL, your interest payment can be deducted from your profits before tax is calculated. This used to be the case for landlords of buy-to-let properties also, but since April 2020 they are only able to claim a 20% tax credit instead which does not offer as much of a tax saving.

- Claim capital allowances for your FHL. Buy-to-let properties are unable to claim for capital allowances where the asset is tied to a particular property and only qualify where it is for general business use. However, this rule for capital allowance does not apply to FHLs and any furniture purchased is an allowable cost deductible against profits. What’s more, with the current Annual Investment Allowance temporarily increased to £1 million until 31 March 2023, now is an opportune time to take advantage and invest in your FHL.

- Claim operating costs as allowable expenses to save tax on your FHL. Capital expenses are not the only costs you can offset against your profits. Additional costs you may incur to run your FHL such as management fees, cleaning and even the utility bills are all allowable expenses to offset against your profits.

- Apply business rates instead of council tax to your FHL. Buy-to-let properties are subject to council tax. Although tenants are often responsible for paying this, if the property is empty then that responsibility falls onto the landlord. FHLs on the other hand are subject to business rates This could amount to a significant financial saving as, depending on the rateable value of your FHL, you could be eligible for small business rate relief which can provide up to 100% tax exemption. You will have to check with your local council to check if you can claim this.

- Profits made from FHLs count as relevant UK earnings for pension contributions. In the UK, there is a cap on how much you can receive in tax relief on pension contributions. Currently it is 100% of your relevant earnings up to a maximum of £40,000. Relevant earnings include your salary, trading income, patent income and income from FHLs but excludes rental income from buy-to-lets. This means that if your salary is £25,000 a year and you receive rental income from a buy-to-let of £10,000, you will still only be able to contribute a maximum of £25,000 in a year. However, if the £10,000 were earnings from an FHL then you would be able to make a maximum contribution of £35,000 in a year.

- No National Insurance (NI) contributions need to be made on earnings from FHLs. Unlike all the other revenue streams that also qualify as relevant earnings as outlined above, profit made from your FHL is the only income which is not subject to NI contributions. There is a temporary NI increase of 1.25% due to begin April 2022 which means the tax saving will be even more substantial going forwards.

- Choose how to split earnings with your spouse. If you own the FHL together with your married or civil partner, you can be flexible with how you split the profits. This can be incredibly useful, especially where one of you is in the higher or additional income tax band and the other is in the basic income tax band. Whereas, if you jointly owned a buy-to-let property, rental profits must be split according to the legal ownership split of the property.

- Benefit from Capital Gains Tax (CGT) relief if you’re disposing of your FHL. There are various options to save tax when it comes to disposing of your FHL. If you sell, you would normally be liable for 18% or 28% CGT depending on your income tax band, however this can be reduced down to 10% where you are eligible to use Entrepreneurs’ Relief. To qualify, you must be able to show that the sale of your FHL forms part of the sale of your business. Other CGT reliefs that could apply to FHLs are Rollover relief or Holdover relief which means that, although there is a transfer of your FHL to another party, the CGT does not arise until the new owners come to dispose of it.

It is important to note that, with regards to the allowable expenses, where there is any personal use of the FHL, only a proportion of the costs will be claimable. For example, if you use the FHL for yourself or for your friends 25% of the time in a year then only 75% of the expenses will be deductible against your profits.

How to pay tax on income from furnished holiday lets

In order to pay tax on the profits made from your FHL you will need to complete a self-assessment tax return annually by the 31 January as well as pay the tax owed. Your self-assessment tax return is also where you’ll be able to claim for all allowable expenses or claim tax relief if relevant to your situation. If you have made a loss on your FHL then you will need to carry this forward to offset against any future profits made on the FHL. You cannot offset the loss against other income. For help completing your self-assessment tax return and ensure you have utilised all allowable deductions to save on tax for your FHL, please get in touch or use the contact form below.

Stay up to date

If you liked this post or found is useful, why not sign up to our monthly email newsletter? Easy reading, the latest news and information, delivered direct to you.

Sign up now

Looking for some help?

If you’re ready to hire an accountant, then get started by completing our contact form for an introductory call to discuss your needs.

You can find out more about our range of Tax Advisory areas.

Related articles

We hope you enjoyed reading this article. If you would like to read

similar posts on this subject here are some more for you.

Back to Tax Guides Home